Expert Interview: SmarTech Analysis’ Vice President of Research Scott Dunham on the Key Trends Shaping the Additive Manufacturing Industry [Part One]

Check out the second part of our interview with Scott Dunham here.

Scott Dunham, Vice President of Research at Smartech Analysis

With the additive manufacturing industry moving at a rapid pace, having the latest data and insights into the market is crucial. SmarTech Analysis is a leading market research firm offering industry analysis and market forecasts specifically for the additive manufacturing industry. The company’s research, forecasts and reports provide valuable insights for companies offering solutions across the spectrum of AM, from hardware and materials to software and services.We were fortunate to speak with Scott Dunham, SmarTech’s Vice President of Research, to discuss the latest trends within additive manufacturing, including the emerging industries to watch out for, the future of the service provider market and what the global outlook for the AM industry looks like.

Could you tell me a bit about your background and how you became involved in additive manufacturing?

I've been involved in additive manufacturing professionally for seven and a half years.

I became interested in 3D printing during my work for a market analyst firm specialising in two-dimensional printing technologies. The market was fairly mature, so the business was looking to expand its coverage into other areas that they thought were related. At the time, I started looking into 3D printing technologies to see if there were any potential similarities. Ultimately, I set out on my own and connected with the president of SmarTech Analysis. At the time, the president of SmarTech Analysis had the idea to start a dedicated market analysis company for 3D printing. We officially started SmarTech at the end of 2013, but it had already existed for about a year at that point in an early startup mode. Since then, it's been really exciting to watch the industry grow and develop over the years.

Could you tell me a bit more specifically about the work you do at SmarTech?

Absolutely. As the Vice President of Research, I oversee, conduct and manage all of the research initiatives that SmarTech is involved in.

At SmarTech, most of the market may know us for the reports we publish, known as syndicated market research studies. But that's not all we do. For example, we’re increasingly involved in collaborative consulting with companies in the industry. We've been fortunate enough to work with most, if not all, of the leading companies in the industry. I'm very involved in overseeing and executing those, and also designing the research methodology to achieve the different goals of the clients. Typically, SmarTech provides some form of opportunity analysis and related consulting. We don't have an engineering background here, meaning that we're not helping to develop new print technologies at a technical level. Instead, we help companies define market opportunities, set market strategies accordingly and provide an in-depth look into the real nitty-gritty details of the business side of the industry to help figure out how things work. We present that information in a logical, often visual, quantitative manner. We also provide advisory services, where we offer quarterly market growth or tracking data to typically larger companies that have a vested interest in receiving ongoing intelligence in the industry. I still also author and directly oversee some of our bigger report titles where we try to quantify the different areas of the market and put out the ever popular projections and forecasts on revenues that will be generated from various areas in the 3D printing industry.

What are some of the ways you've seen the additive manufacturing industry change over the years?

There are definitely elements of things that have changed and things that have stayed the same. For example, the topic of industrial 3D printing for manufacturing — anything that could take the industry outside of the rapid prototyping bubble — that was being talked about even seven years ago.

The print processes remain largely the same at a technical level. What really has changed over that period of time is the things that enable companies to use 3D printing for production rather than just for modelling and prototyping at a low level. These include workflow automation software and all the other software elements, especially on the post-processing side, which has seen a huge leap forward. The advancements in these areas help to overcome the challenges companies face using largely the same technologies but for different goals. Those areas become heavy cost centres when a company tries to scale up. It’s the areas where things start to break down when it comes to volume production. You have to really manage those and reduce the pre- and post-processing burden.We're starting to see some interesting changes in the architecture of certain machines. The machine architecture starts to alter to help support that manufacturing-induced goal. Let’s take metal powder bed fusion systems as an example. If you look at what was being marketed and sold for manufacturing seven years ago, you’ll see that it was the laboratory style machines, where you had to manually put the powder in the machine and let the machine cool down, before taking the printed part out of the remaining powder. Then before you could start another job, you had to reload the machine with powder, and so on. Obviously, that's a fairly inefficient process. To help increase the overall productivity and therefore reduce the cost of individual parts, now it's very common to have a machine architecture where you have individualised material and laser processing stations. With this machine architecture, you pull the material out, put a new, pre-prepared material station into the printing module, and it continues printing, while you're off getting the part out of the powder and post-processing it. This approach allows you to have a much more continuous cycle of operation. So it’s still the same processes. They're being refined here and there in a step change manner but the real things that are changing are these other areas that are supporting the processes.

We often hear about 3D printing being used in key industries like medical and aerospace. Are there other industries where you're seeing an increasing adoption of the technology?

Aerospace and medical have been the most established industries when it comes to adopting 3D printing. But the growth rates within these industries are lower today when looking at factors like the compounded annual growth rate of the amount of hardware sold into a specific industry. That's because these industries have historically been more established and they're simply not going to keep growing at the same or increasing rates over time.

There's still plenty of growth left in aerospace and medical. But when looking from the perspective of what's growing fastest and what could rise quickly and become on an equal scale with aerospace or medical, automotive is definitely in the conversation. We should also really keep an eye on the various areas within the consumer goods industry, as well as collective energy industries, like nuclear and oil & gas. Consumer products is a very broad market and we're seeing a lot of really interesting use cases coming out of companies like Carbon, Desktop Metal, and even the more established ones, like EOS and 3D Systems. We’re not talking about huge, hundred thousand parts per year type of applications just yet. But what we're seeing is that these applications, which were considered much more fringe previously, are starting to be investigated from the perspective of how 3D printing can be integrated into manufacturing beyond modelling, prototyping and product development. Carbon has a great case study with Vitamix, a blending equipment manufacturer. Blenders are a relatively mundane type of consumer product, but have really big potential in terms of volumes. That specific company is seeing a lot of return on investment for just reengineering a couple of parts in one of their products on one of their popular product lines. Things like that are really going to drive the growth of the technology in this industry in the future. There's plenty of room left to grow in medical and aerospace, but at some level other areas like consumer products have significantly greater potential.

Are there any examples of very niche verticals where 3D printing can still play a transformative role?

Oil and gas is definitely one. Electronics is another. There are a lot of processes that are additive in nature, and they exist exclusively to serve electronic applications. We view those almost as a separate area of the additive picture. Technically they are additive, but in many ways, you're talking about deposition of really small amounts of material and still in almost two and a half dimensions instead of three dimensions. But that's not to diminish what's going on there. Of course, there are areas of consumer electronics that are not just circuit boards. There are injection moulded type of parts that are integrated into consumer electronics, that could be great candidates for 3D printing technologies. So electronics is certainly an area that we're watching closely.

One thing that is really interesting to me and that I think is a great indicator of the potential for adoption across many markets is the 3D printer manufacturers themselves using the technologies to produce parts for their hardware or other applications. HP has been very public about that, essentially printing parts to put into its Multi Jet Fusion printers. Renishaw produces a portion of their optical control system out of metal parts that were redesigned for additive. When you look at it from that perspective, that's like a great measure of putting your money where your mouth is. These machines are maybe not being sold in huge volumes — we're talking about several hundred or maybe up to 1000 machines per year — but that's getting into some serious production volumes at the part level. If they're willing to trust their technologies for these applications, that's a great case study to take to other industrial manufacturers and say ‘look we're doing this in our own products already, so there's nothing really stopping you from investigating it for similar use cases.’3D printing parts for 3D printers first started in the low cost desktop area with the RepRap project many years ago. To see it come up to the industrial level now in a much more serious manner and across a number of different manufacturers is particularly exciting.

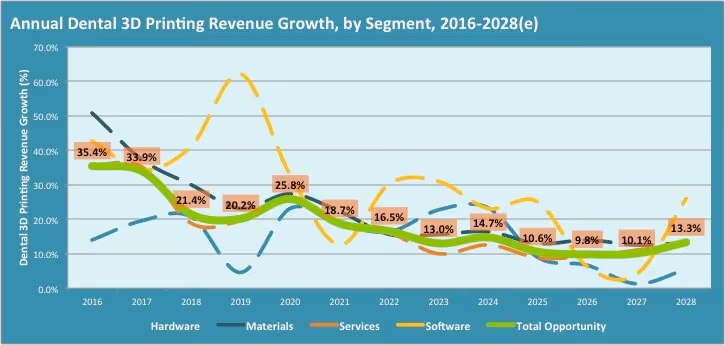

Recently, SmarTech issued a report on the on the dental market. Could you share some of the top findings from that report for our readers?

[Image source: SmarTech Analysis]

Absolutely. If you've been following this for any length of time, you may have noticed that the marketing around 3D printing in dentistry has increased quite a bit over the past few years. The dental market has become a serious target for many of the technology developers around 3D printing. When you look at it, dentistry is not that big of a global opportunity, compared to some of the other areas that 3D printing is chasing. So why everybody are so hyped up or focusing their marketing efforts and their solution development around dentistry? The reason is the potential to convert that entire industry’s production capacity to additive versus either the traditional manual, analog solutions, or subtractive digital technologies. There are not very many industries out there you can say that about. Everybody likes to talk about the hearing aid industry and how close to 100% of all hearing aids are now 3D-printed. But that’s actually a flawed case study. The whole case about ‘all hearing aids are 3D printed’ is not true at all. For a short period of time they were, when the industry was very focused on producing customised products. But for the last several years, hearing aids companies have been pushing non-customised products for a number of reasons. And there's not a great value proposition to print non-customised hearing aid shells. Dentistry is bigger than the hearing aid industry. In dentistry, you could, in theory, have a great case for converting 80% plus of the means of production to an additive technology, and there's no going back from that. I think in many cases it will surpass the milling technologies and the use case for milling technologies will be significantly reduced in time. There's already a great demand for digital processes in dentistry overall, regardless if they're additive or subtractive. There’s a demand to convert what has been a manual, very expertise and skill-driven production process to something that's digital, repeatable and has all those benefits that digital processes offer. There's already a good appetite out there and it's growing pretty quickly. Certainly not everywhere around the world, but especially in the United States, in the Western European markets, and even in Asia. On the other side, you have an increasingly compelling value proposition for the use of 3D printers that are able to print a really wide range of dental devices and restorations now with more or less just a material change. So you can have one system and produce things with significantly less material waste. Milling machines definitely provide a really good solution, but they do have limitations when it comes to meeting the actual needs of customisation for things that go in your mouth. So additive is really growing based on those factors. That is really going to bring it to the next level and get to that point of transitioning the whole industry over to additive or the next generation of dental 3D printing technologies that are just starting to come to market. In particular, you have 3D printers from 3D systems, Carbon and EnvisionTech. All of them are using photopolymerisation techniques; most people call it Stereolithography (SLA) or resin-based printing. These companies now have layerless and continuous printing processes using resin materials. Fairly quickly, we've seen that photopolymerisation 3D printing converted over to being able to use most, if not all, of the dental materials that people are comfortable within the industry. There are just so many benefits to those processes within the dental industry, from high productivity to what could truly be one-visit dentistry. You could print a surgical guide, or maybe even a temporary restoration in just a couple of minutes and throw a few minutes for post-processing. These technologies can help to eliminate the need for the post-processing that the dental industry has become used to, although it slows down the productivity and creates some hassle for in-office use. But these next-generation technologies have the capability to significantly reduce even those requirements. That's really going to play a huge role in that transition over to entirely additive means of production in dentistry.

What does the AM market look like in non-European and non-US territories? Is the rate of adoption very different?

There's a great long term outlook. Asia is quite advanced in certain areas. Looking at it from a quantitative standpoint, like we tend to do at Smartech, Asia is already a sizable opportunity. But there's a lot more potential left untapped.

However, if you get into the Middle East, Africa, South America, the adoption is much further behind and at a lower level. What has penetrated those areas is the lower-cost machines. As far as how it looks from one region to another, the adoption of additive tends to follow different trends there. But overall, the actual concentration of the industry is split between North America, Europe and Asia. A lot of people tend to think that Asia is an emerging market and it's further behind, but there are fast growth and long, great potential. That said, there are many companies concentrated specifically in China and Japan, which haven't necessarily had a big impact on the global scale. But within that region, there's a lot more happening than people in the West realise when taking a quick glance at things. There are a lot of printer companies out there trying to capitalise on the opportunity. But there's also a growing presence of service providers in that area, utilising 3D printing in a more advanced way. Rapid prototyping has been concentrated in Asia for a long time. Increasingly, the North American and European AM companies are establishing serious service relationships in Asia. They are definitely heavily focused on that area for future growth, for a number of different reasons. These companies are targeting outsourced manufacturing, which is already a part of the industries. Following that out to where it lives in is definitely one of the reasons.

To learn more about SmarTech Analysis, visit: https://www.smartechanalysis.com/

.avif)

.svg)

Subscribe to our

newsletter