Additive Manufacturing Around the World: What is the State of 3D Printing Adoption in North America and Europe?

Chech out Part 2 of AM Around the World series, which explores the adoption of3D printing in the APAC region.North America and Europe remain the two regions with the largest share in the additive manufacturing (AM) market. A considerable number of companies developing, adopting or investing in AM are headquartered in these regions, making them hotbeds of technology advancements. At the same time, however, North America and Europe could be at risk of losing their role as leaders in AM to the rapidly growing AM market in Asia. So how is the 3D printing industry evolving in these regions? And what should North America and Europe do to secure their competitiveness?

3D printing adoption in North America

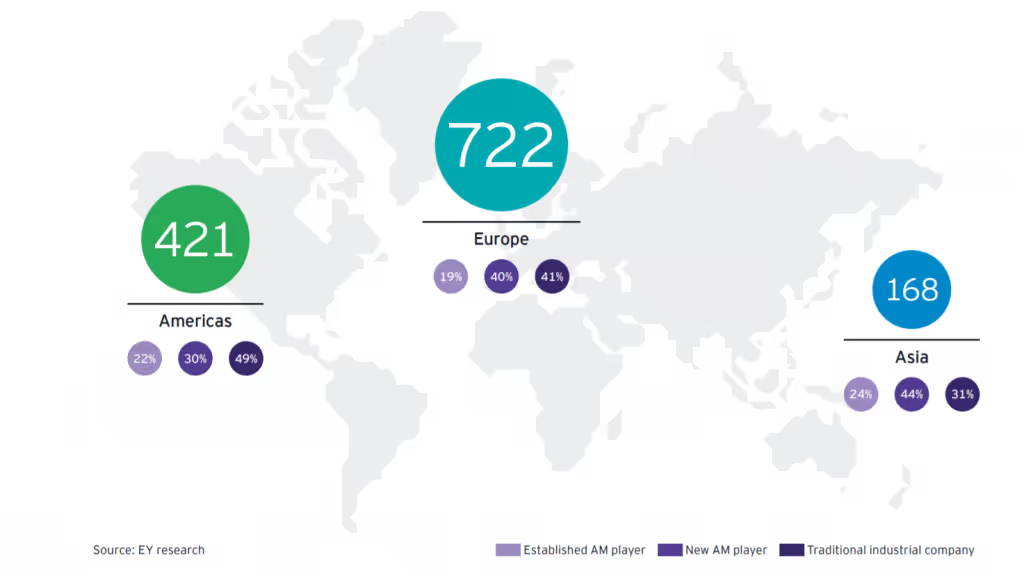

The North American region continues to dominate the AM market. According to the Wohlers Report 2019, North America has the largest share (35 per cent) of installed industrial AM systems. Much of this share comes from the United States. The US remains the global leader in 3D printing, thanks to its early development of the technology and historic leadership in traditional manufacturing. The growth of the technology in the region is also supported by the number of key industry players and the leading number of patents. According to report by EY, 29 per cent of all AM companies are headquartered in the US - the highest number globally. Among them are established players like 3D Systems and Stratasys, the trifecta of unicorns (Carbon, Desktop Metal and Formlabs) and a large number of traditional manufacturing companies that have made the leap into AM (e.g. GE and HP). Also, interestingly, US-based 3D printing companies get the most venture capital (VC) investment. In the first half of 2018, US-based 3D printing start-ups raised over $600 million - more than the money raised from 2012-2015 combined, according to data from Pitchbook.

The role of the US government in AM industrialisation

While private investment has been the primary innovator in 3D printing in the US, there’ve been a few transformative government initiatives. One of these is the launch of the National Additive Manufacturing Innovation Institute (NAMII) in 2012, which serves as the national accelerator for AM. A year after its founding, NAMII was rebranded as America Makes. Today, America Makes is a recognised hub of advanced manufacturing innovation, with 88 AM R&D projects executed. It has evolved from a membership community of 65 founding organisations, to more than 225, as of 2019. One of the greatest achievements of America Makes is the collaboration with American National Standards Institute (ANSI) on the creation and publication of the first Standardisation Roadmap for AM.The roadmap is designed to identify standards (approved and under development), assess gaps and determine priority areas for additional R&D and standardisation. A lack of standards remains one of the key barriers to accelerating AM adoption. With a standardisation roadmap, standard developing organisations can have a clearer picture of the current standards landscape and can prioritise standards development in areas that need them the most. Ultimately, the roadmap works as coordination document, facilitating the development of a consistent and harmonised set of AM standards.

Is the US losing its edge in AM?

Despite its leading position in AM, the US could be at risk of losing ground to other regions. According to an analysis by A.T. Kearney, challengers like South Korea, the UK and Germany, could outpace the growth of AM in the US within the next few years. For one, the country lacks a nation-wide strategy for AM. According to an analysis by A.T. Kearney, the US had lower government support of 3D printing in 2017 when compared to the leader’s average in AM government engagement. As of 2019, not a lot has changed in this regard. Although the White House released an updated Strategy for American Leadership in Advanced Manufacturing report in October 2018, the report doesn’t indicate any official policy change on AM. That said, there have been some notable government investments in AM in recent years. In 2016, the U.S. Air Force granted Aerojet Rocketdyne, an American rocket and missile propulsion manufacturer, $6 million to develop standards for 3D-printed rocket engines. This grant was intended to reduce U.S. reliance on foreign-made launch vehicle components. Furthermore, the 2018 US military budget included the $13.2 billion support for technology innovation, including 3D printing. The 2019 military budget has allocated resources for defence-related 3D printing research as well. Despite this funding, initiatives that apply AM beyond aerospace and defence are seeing much less support.

Private companies are driving the AM industry

In 2019, AM is becoming more pervasively adopted across US shop floors. More than half of US companies are applying 3D printing, and 22 per cent are considering adoption in future, according to the EY report. Companies from aerospace, industrial goods and medical sectors, are making AM one of their key investment and research areas. There is also a strong upward trajectory for AM in the US automotive industry. For example, Ford has invested $45 million into its new Advanced Manufacturing Center and has begun printing functional parts for some of its vehicles. GM is also developing approaches to using AM for its future electric cars. Interestingly, North American companies are more optimistic about the potential of 3D printing than European ones, states a 2019 Sculpteo report. More than half of the surveyed North American companies plan to increase their investment in AM by at least 50 per cent.

Private companies’ commitments are fuelling the growth of AM in the US. However, to maintain its leadership position, the US government needs to be more involved in the AM ecosystem. US policymakers should consider implementing a broader program of initiatives around AM workforce development, education and incentives for companies to adopt 3D printing.

3D printing adoption across Europe

After North America, Europe has the second largest AM market share.It is home to a large number of established industry players, with a strong history of technical expertise in AM processes, including the likes of EOS, Renishaw, SLM Solutions, Ultimaker and Photocentric. In fact, Europe is the region with the most (55 per cent) AM firms, followed by the Americas with 32 per cent and Asia with 13 per cent, according to a report by EY.

The majority of the 3D printing companies are centred in Western Europe, with countries like Germany, the UK, Italy and France driving AM development and applications. According to a survey by IDC, these countries are also leading the way in the adoption of AM for end parts, particularly in the aerospace and healthcare industries. Some of the countries have also developed a national strategy for AM as a part of their advanced manufacturing and Industry 4.0 plans. While Western Europe has taken the lead in the adoption of industrial 3D printing, Eastern Europe is still lagging behind. The Russian Federation, the biggest economy in Eastern Europe, has huge potential for 3D printing but needs a lot of R&D to identify suitable applications and implement relevant solutions. Many of the Russian government’s corporations have announced programs for developing industrial technologies like AM. However, taking them onto the manufacturing floor still represents a key challenge.In fact, many European companies are facing challenges when it comes to adopting 3D printing. A 2018 report, conducted by CECIMO, the European Association for the Additive Manufacturing industry, states that skills shortage remains one of the region’s key challenges. 52 per cent of respondents reported having struggled in the recruitment of competent AM staff in the recent past. That said, CECIMO’s report also identified the most sought-after areas of AM know-how for European AM adopters. These include aspects like quality assurance and testing, and knowledge of regulatory approval procedures – of which all are indicative of the increasing presence of AM in series production.

Country Spotlight: Germany

The largest manufacturing country in the EU, Germany, also has a top position when it comes to the adoption and industrialisation of AM. As early as 2011, the German Federal Government launched the ‘Industrie 4.0’ initiative, which included the focus on 3D printing, among other digital technologies.One reason Germany is targeting 3D printing as a key technology, is to maintain its competitive advantage in the global arena. For this, Germany allocates funding and develops specific policies and institutions. It’s estimated that there are 148 research institutions distributed across Germany, which are active in the field of AM. The Fraunhofer Research Institute is perhaps the biggest among them. The Fraunhofer InstituteIn 2017, the Fraunhofer Institute, together with 6 partners, launched the FutureAM project. The project aims to accelerate metal AM by developing technological solutions that will help to increase the scalability, productivity and quality of AM processes for the production of metal components. At this year’s Formnext, the team members will showcase project results, which could be transformative for the industry. For example, one of the results involves the development of a new, compact optical system for Laser Powder Bed Fusion (L-PBF). The first prototype of this system is now in use and, with a build volume of 1000 mm x 800 mm x 500 mm, is said to produce large metal components up to 10 times faster than conventional L-PBF systems.The Additive Manufacturing AssociationThe Additive Manufacturing Association within VDMA, the German Engineering Federation, is also highly involved in AM industrialisation.In the 5 years of its existence, the Additive Manufacturing Association has grown to around 150 members. These include leading suppliers of AM production technology for processing metals and plastics, suppliers of components, software, automation technology and materials, as well as industrial users from various industries and leading research institutes.Last year, members of the Additive Manufacturing Association began compiling a roadmap, sketching out the way to automate manufacturing processes for industrial 3D printing. In its research, the association identified R&D issues in materials logistics, the environmental, health and safety area, data processing and process standardisation. In order to resolve them, the association encourages research groups to come together and share the experience and know-how of different sectors and industries. More recently, Siemens announced a new 3-year project, called Industrial Implementation of Digital Engineering and Additive Manufacturing (IDEA), as part of the ‘Line Integration of Additive Manufacturing processes (LAF)’ funding initiative, created by the German Ministry of Education and Research. The priority for the 3-year project is to ‘further industrialise AM for Germany’s industrial sector’ by improving the link between hardware and software through digital twins. Projects like these will be key drivers to accelerating industrial use cases of AM. Currently, only around 13 per cent of 560 German companies surveyed by VDI, the largest engineering association in Western Europe, are using AM for the production of complete end-use products. However, one third states that they manufacture products with some components 3D-printed – which is an encouraging trend. When it comes to industries adopting AM in Germany, automotive is one of the fastest-growing ones. There’ve been a number of projects and initiatives aimed at bringing the advantages of 3D printing to automotive applications.One of the most promising is an ‘Industrialisation and Digitisation of Additive Manufacturing for Automotive Series Processes’ project, IDAM for short. Launched by BMW Group earlier this year, the project aims to deliver at least 50,000 components per year in mass production, using AM, and over 10,000 individual and spare parts.If successful, IDAM could become a milestone for the introduction of serial AM into the automotive industry. Clearly, 3D printing has become a matter of national importance in Germany. Considering the huge support from the government, institutions and private organisations, Germany is well-positioned to remain a 3D printing leader in Europe for the years to come.

Country Spotlight: the United Kingdom

The UK is amongst the global leaders, in both the development of knowledge and successful application of AM technology. According to research by A.T. Kearney, the UK is the second-largest supporter of 3D printing in Europe, after Germany. The UK has been well placed to take advantage of AM, having been an adopter of the technology during the 1990s for rapid prototyping applications.As 3D printing has evolved, the UK has seen a strategic opportunity for AM to help revitalise its manufacturing economy and be more competitive on the world stage.In early 2014, talks began on establishing a national strategy for AM. In 2017, the government published an Industrial Strategy, giving a clear route to making the UK a leading player in AM.One of the country’s strengths lies in AM research and development. Several leading UK universities are actively engaged in AM-related research, with the three largest centres of research activity being the University of Nottingham, University of Sheffield and the University of Cambridge.Furthermore, the Manufacturing Technology Centre (MTC), opened in 2015, houses one of the most advanced National AM Centres.

However, while the UK has considerable capacity in research, commercial adoption of the technology in manufacturing is still slow. Some companies are using AM to a great extent, such as Bowman International for bearing cages, Renishaw and Attenborough Dental for crowns and bridges, Metron for elite cycles, Croft for filters and GKN for aerospace and automotive components. However, the vast majority of the UK industry has yet to fully adopt the technology.‘Lack of skills and specialist training, lack of understanding by government, an overly cautious investment attitude and confusion about ROI among business owners, and a fragmented business support structure’, have been identified as key barriers to the adoption of AM in the UK. Although there’s a lot of support for businesses from multiple AM centres, a crucial part – educating and persuading engineers on the production line – is lacking.That said, the UK has the potential to build a strong knowledge-based AM supply chain, with the presence of enabling software and hardware companies, material providers developing innovative product offerings, and world-class product designers with a strong interest in AM. Ultimately, the growth in AM will mainly be application-driven, and there is no reason to believe that the UK cannot benefit from this, given its strong knowledge-intensive manufacturing base.However, there’s a strong need for government involvement to co-ordinate a fragmented AM community to develop approaches, particularly top-down, to overcome challenges to adoption.In summary, the UK has the experience and capacity to both develop new AM processes and apply existing technologies. However, today it’s more important than ever to develop and fund initiatives that will translate research into a commercial AM usage among the greater number of companies.

3D printing in North America and Europe: Maintaining a competitive edge

In 2019, North America and Western Europe remain at the forefront of the 3D printing industry. Both regions allocate financial resources to develop AM technologies and applications, with Germany and the US driving the majority of advancements in AM. That said, the global economic and political climate creates a lot of uncertainty for European and North American regions. Brexit and the US trade war with China, which disrupted key trading relationships and caused the manufacturing sector of major global economies to shrink, are affecting the pace of growth of the AM market in both regions. However, Europe and the US are willing to co-operate with each other to further the industrialisation of the technology. The EU recently declared a commitment to prioritising AM in trade talks with the US for industrial goods. The decision will seek to address existing non-tariff barriers in the EU-US trade of AM solutions, which have posed financial and administrative burdens on exporters. In the most recent January 2019 update on these discussions, the Commission submitted 2 potential agreements, pending approval from the U.S.Accepting these 2 agreements would benefit both parties, as it would effectively create a singular-standards track for companies in the EU and the US, eliminating the need to reapply for certification when entering a new geographic market. For AM, in particular, this would alleviate the burden of resources currently needed to obtain multiple, practically identical, certificates. As a result, companies would be able to redirect efforts and focus more on the technology maturation. This could potentially be most beneficial to highly regulated industries such as aerospace, medical and automotive.While initiatives like these are crucial, companies and policymakers, alike, must also focus more on fostering AM education and building incentives to attract the use of 3D printing. North America and Europe are at risk of losing their seats at the head of the global 3D printing industry, with Asia fast becoming a strong 3D printing competitor. It means that now is the time for both regions to take the actions needed to establish a robust and comprehensive AM ecosystem that will propel them into a new era of digital manufacturing.

.svg)

Subscribe to our

newsletter