40+ 3D Printing Industry Stats You Should Know [2021]

A collection of 40+ relevant 3D printing statistics and facts looking at the current state of the industry

The 3D printing industry is evolving and developing rapidly, making it difficult to keep up to date with the trends in this space. A great way to stay up to speed is to keep an eye on 3D printing statistics.

To ensure that you keep up with the latest in the industry, we’ve compiled a list of relevant 3D printing statistics, highlighting the recent growth and evolution of the industry, alongside a succinct analysis of the key industry segments.

[toc]

The current state of the industry

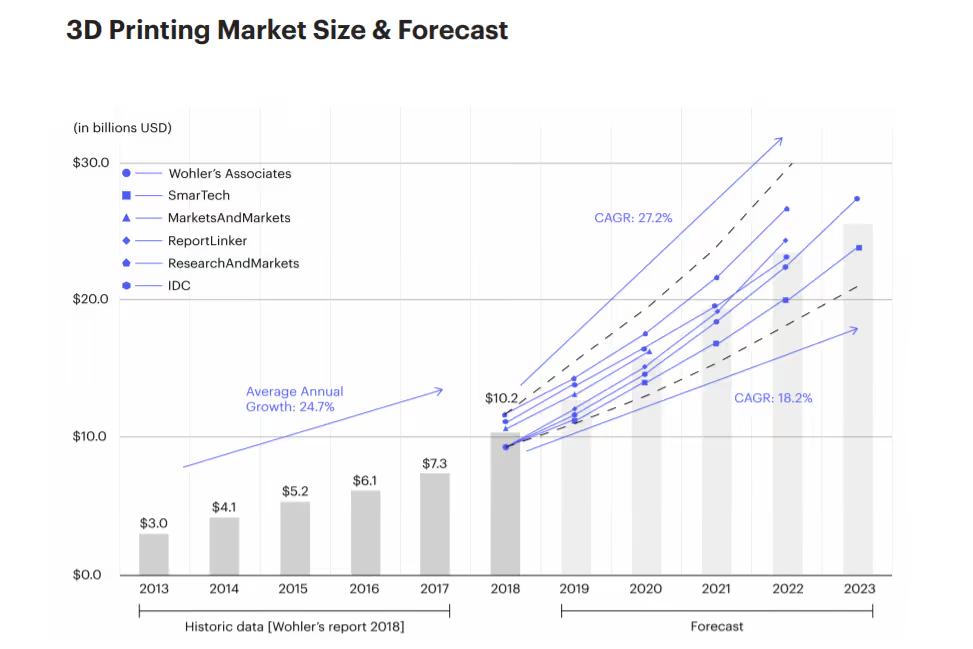

The 3D printing industry has been on a stable growth path over the last decade. Although 3D printing is still less than 1 per cent of the global manufacturing market, the technology is set to become an invaluable tool for production workflows.

It means that the perception of 3D printing, as a solely prototyping technology, is changing, and not it's perceived as a rapidly maturing manufacturing solution.

1. In 2019, the global additive manufacturing market grew to over $10.4 billion, crossing the pivotal double-digit billion threshold for the first time in its nearly 40 year history. (SmarTech Analysis, 2020 Additive Manufacturing Market Outlook and Summary of Opportunities Report)

2. In 2018, VC funding exceeded $300 million in start-ups related to 3D printing. The common thread of all investment: industrial solutions and applications. (Hubs, The 3D Printing Trends Report 2019)

3. The 3D printing market is set to double in size every 3 years with the annual growth forecasted by analysts varying between 18.2 and 27.2 per cent. (Hubs, The 3D Printing Trends Report 2019)

4. 71 per cent of companies say that a lack of knowledge is the greatest factor on project-by-project choices to use 3D printing or traditional methods, while 29 per cent insist that it’s a lack of confidence in 3D printing as being reliable. (Jabil, A Survey of 3D Printing Stakeholders in Manufacturing 2019)

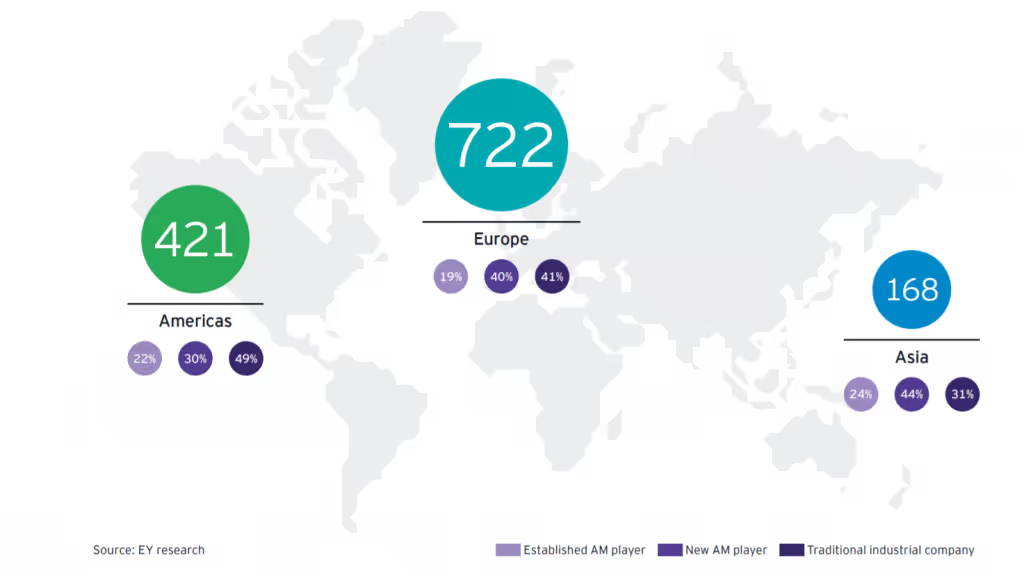

5. Based on the number of industry players, systems manufacturers make up the biggest group in the AM market (38 per cent), although the number of service providers has risen dramatically, reaching 34 per cent. (Ernst & Young, 3D printing: hype or game changer? A Global EY Report 2019)

Adoption

Many industries are embracing 3D printing to make better products faster and to optimise their operations. However, adoption rates vary across sectors. Companies within the aerospace, medical, automotive and industrial goods industries are among the most mature adopters of the technology and also key contributors to the industrialisation of 3D printing.

In the meantime, the adoption of 3D printing is also uneven across geographical regions. Currently, North America and Europe lead the charge. However, the two regions are at risk of losing their seats at the head of the global 3D printing industry, with Asia fast becoming a strong 3D printing competitor.

6. In 2019, footwear 3D printing revenues made up approximately 0.3 per cent of global footwear market revenues, according to SmarTech Analysis. (SmarTech Analysis, Markets for 3D Printed Footwear 2019 Report)

7. The orthopaedics 3D printing market was valued at $691 million in 2018 and is predicted by SmarTech Analysis to grow into a $3.7 billion market by 2027.

8. The market for medical 3D printing, including materials, services, software and hardware, is currently estimated to be worth $1.25 billion, according to SmarTech Analysis.

9. A report by SmarTech Analysis suggests that revenues for 3D-printed dentistry will grow to $3.7 billion by 2021, and the technology will become the leading production method for dental restorations and devices worldwide by 2027.

10. The USA, UK, Germany, France and China are the top 5 countries with the highest 3D printing adoption and investment rates. (Ultimaker, 3D Printing Sentiment Index)

11. Germany generated around €1 billion in AM-related revenues during 2019.

12. The US has the largest installed base of 3D printers of 422,000 units in the world. (Ultimaker, 3D Printing Sentiment Index)

13. The number of surveyed organisations with AM systems in-house more than quadrupled in the past 3 years, leaping from 9 per cent in 2016 to 40 per cent in 2019. (Ernst & Young, 3D printing: hype or game changer? A Global EY Report 2019)

14. AM adoption is growing across shop floors globally, evidenced by more than 70 per cent of enterprises finding new applications for 3D printing in 2019 and 60 per cent using CAD, simulation and reverse engineering internally. (Sculpteo, The State of 3D Printing Report 2019)

Applications

The primary use of 3D printing remains in the realm of product development. Yet, the stats below show that increasingly the technology is maturing into a fully-fledged production solution.

In addition to offering greater flexibility in production, 3D printing also enables businesses to create new business models that were previously either not feasible or not economically viable.

Ultimately, the scope of applications and opportunities possible with 3D printing will be increasing in line with the growing capabilities of the technology.

15. Proof of concept and prototyping dominated 3D printing applications in 2019. (Sculpteo, The State of 3D Printing Report 2019)

16. The number of manufacturers using 3D printing for full-scale production has doubled between 2018 and 2019: 21 per cent and 40 per cent respectively. (Essentium, A survey of manufacturers)

17. 79 per cent of surveyed companies expect their use of 3D printing for production parts or goods to at least double in the next 3 to 5 years. (Jabil, A Survey of 3D Printing Stakeholders in Manufacturing 2019)

18. In the aerospace and defence industry, the most popular application of 3D printing is prototyping (72 per cent), followed by repair (44 per cent), research and development (43 per cent) and production parts (39 per cent). (Jabil, A Survey of Aerospace and Defense OEMs MAY 2019)

Hardware

The hardware segment of the 3D printing industry is evolving rapidly, with 3D printers becoming faster, more reliable and production capable.

In terms of technology, the metal 3D printing segment is growing fast, particularly binder jetting and compact metal machines, which tend to be cheaper than Powder Bed Fusion (PBF) systems.

At the same time, polymer 3D printing hardware remains the biggest segment in terms of systems in use. Technologies like Selective Laser Sintering, Multi Jet Fusion and Stereolithography have evolved to the point where they are used in the production of thousands of parts.

Finally, the markets for ceramic and electronic 3D printers remain relatively young. That said, the development of new technologies - for example, XJet’s Nanoparticle Jetting Technology for ceramics and DragonFly Lights-Out Digital Manufacturing (LDM) for electronics – sets the foundation for these markets to reach maturity in the near future.

19. Research firm, CONTEXT, estimates that metal 3D printer shipments will see year-on-year unit-volume growth rates of over 49 per cent.

20. The metal AM hardware segment is set to create an almost $4 billion revenue opportunity by 2024.

21. 62 per cent of the globally installed PBF metal AM systems come from German suppliers. (AMPOWER, Metal Additive Manufacturing Report 2019)

22. In metal PBF processes, 20 per cent to 40 per cent of the raw part costs are associated with material costs. In powder-based DED processes, the material can make up 70 per cent of the raw part cost, in Wire Arc Deposition even up to 80 per cent. (AMPOWER, Metal Additive Manufacturing Report 2019)

23. The global metal AM market was worth EUR 1.51 billion in 2018 and is set to grow at a 25 per cent CAGR. (AMPOWER, Metal Additive Manufacturing Report 2019)

24. The Powder Bed Fusion family plays the largest role in metal AM, comprising 80 per cent of all metal AM system installations worldwide.

25. The sales of compact industrial metal printers will top $1 billion by 2027.

26. 72 per cent of companies, surveyed for EY’s Global 3D Printing Report 2019, are using polymer AM systems, compared to 49 per cent that use metal ones.

27. HP’s Multi Jet Fusion has become one of the fastest-growing polymer 3D printing processes. More than 10 million parts are said to have been produced using MJF 3D printers in 2018.

Materials

The materials market remains a vital part of the 3D printing industry. One of the key trends shaping the market is the increased activity within materials development. In many ways, this trend is being driven by market demand, with customers demanding functional materials, particularly for production applications.

Both large materials companies and niche start-ups are actively developing high-performing materials, be it composites, metals or ceramics. Material prices are also coming down slowly but surely.

These trends taken together indicate a healthy maturation of the materials industry, which is predicted to grow into a whopping $4.5 billion opportunity in the next 5 years.

28. In 2019, the AM materials market was valued at $1.5 billion.

29. 99 per cent of manufacturing executives believe an open ecosystem is important to advance 3D printing at scale.

30. The most commonly used material for 3D printing continues to be plastics, at 82 per cent. Companies using 3D printing are also working with carbon fibre (24 per cent) and composites (20 per cent). (Ultimaker, 3D Printing Sentiment Index)

31. The polymer AM segment grew to an estimated nearly $5.5 billion in 2018. (SmarTech Analysis, A 2019 Additive Manufacturing Market Outlook and Summary of Opportunities Report)

32. Sales of materials for polymer Powder Bed Fusion were at an all-time high in 2018, exceeding $400 million. (The Wohlers Report 2019)

33. The 3D printing ceramic materials market is expected to grow from a $20 million revenue opportunity in 2020 to over $450 million by 2029, according to a report by SmarTech Analysis.

34. 94 per cent of surveyed companies say designers choose traditional manufacturing due to the lack of additive materials. (Jabil, A Survey of 3D Printing Stakeholders in Manufacturing 2019)

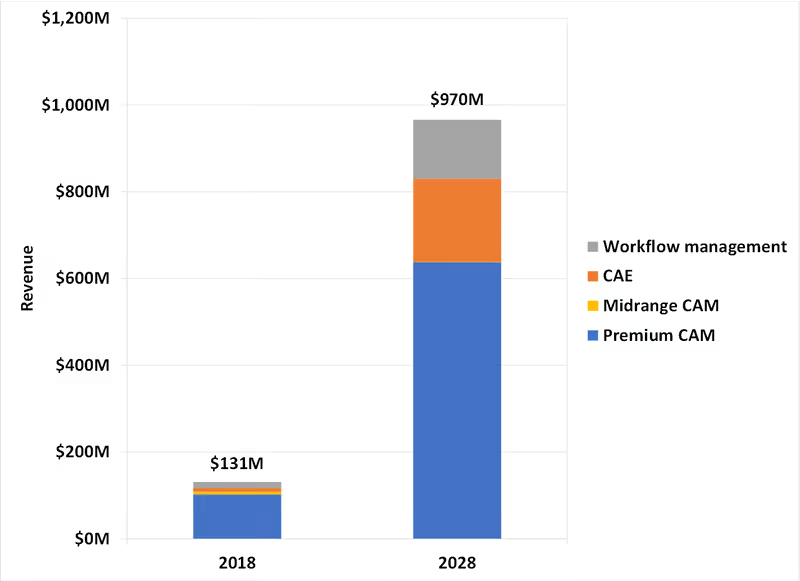

Software

The 3D printing software segment is smaller than the hardware and materials segments. However, in recent years it’s been on a steady growth path, driven by the need to overcome multiple challenges within the 3D printing workflow.

Today’s 3D printing software solutions are unlocking the possibility to create complex designs faster and increase print success rates. In addition to that, ensuring part quality and managing workflows more efficiently have also become possible with the development of a new generation of software products.

As seen on the graph below, the software segment was relatively small in 2018, but it holds huge potential to grow into almost a billion worth of opportunity within the next decade.

Post-processing

As 3D printing moves to production, there’s a great push to overcome post-processing challenges, such as manual operations, which tend to increase lead-time and cost of 3D printing. According to a whitepaper by RIZE (3D Printing: The Impact Of Post-processing), post-processing can add between 17 per cent and 100 per cent to 3D printing time on a batch-by-batch basis.

A number of companies have appeared on the market in order to tackle post-processing challenges by developing automated solutions for part cleaning, depowdering, surface finishing and dyeing.

35. 66 per cent of companies report experiencing 2 or more challenges with their current Post-Printing. (PostProcess Technologies, 3D Printing Trends Report: Additive Post-Printing Survey 2019)

36. 75 per cent of companies indicate Length of Time to Finish Parts as a key challenge in their Post-Printing, while for 51 per cent of respondents, the challenge lies in a lack of consistency. (PostProcess Technologies, 3D Printing Trends Report: Additive Post-Printing Survey 2019)

Service bureaus

Service bureaus represent a big part of the AM market. According to the EY Report 2019, service providers make up 34 per cent of the global AM landscape. And the percentage is set to grow. By 2022, nearly one-third (32 per cent) of 900 surveyed companies expect to design and produce their AM parts via service providers.

The key reasons for companies to use service providers are the reluctance to invest in their own equipment, lack of experience and skills, as well as the opportunity to produce parts on-demand and closer to the point of use. The latter, in particular, could be the driver behind the rise of online 3D printing services, like Hubs and Sculpteo.

37. Small and medium-sized enterprises (SMEs) are the power users of online 3D printing services, representing more than 75 per cent of the global customer base. (Hubs, The 3D Printing Trends Report 2019)

38. The industry most commonly served by 3D printing service bureaus is consumer goods (with 77 per cent of respondents choosing this option). In second and third place are automotive (75 per cent) and industrial goods (73 per cent). (AMFG, AM Service Provider Report 2019)

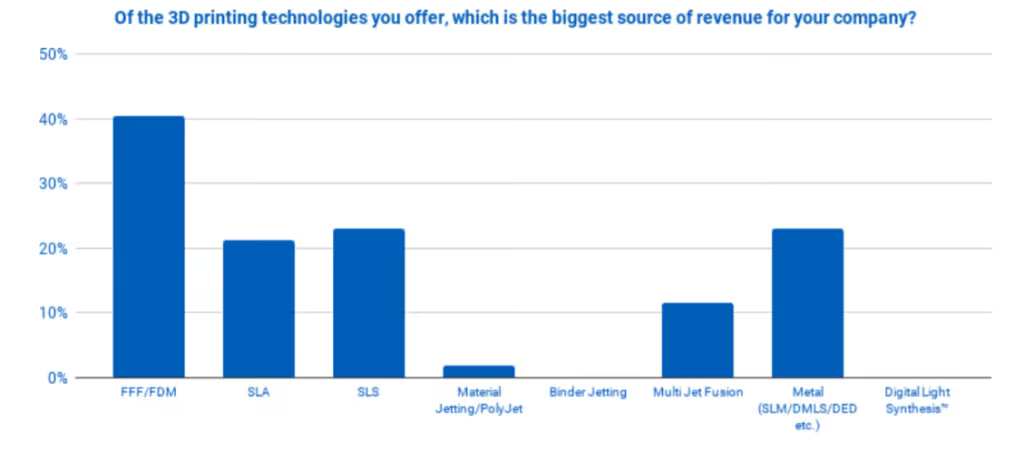

39. FFF/FDM, SLA and SLS are the technologies most commonly offered by AM service providers. (AMFG, AM Service Provider Report 2019)

40. 37 per cent of 3D printing service providers reported producing between 1,001 and 10,000 parts annually. This was followed by a quarter who reported producing between 10,001 and 50,000. (AMFG, AM Service Provider Report 2019)

41. The number of companies using service providers has more than tripled from 8 per cent in 2016 to 26 per cent in 2019. (Ernst & Young, 3D printing: hype or game changer? A Global EY Report 2019)

42. Around 81 per cent of companies cite a reluctance to invest in their own systems as their reason for working with service providers in the future. 48 per cent cite their unfamiliarity with AM processes and standards, while 38 percent cite their uncertainty around AM design. (Ernst & Young, 3D printing: hype or game changer? A Global EY Report 2019)

3D printing statistics: A tale of the burgeoning industry

The 3D printing industry is becoming bigger and more mature year on year. And the statistics above make this trend especially evident.

Of course, the industry, as it penetrates more markets and verticals, still needs to overcome a number of challenges. Spreading the knowledge about the true capabilities and limitations of the technology, as well as making it more accessible to small and medium-sized companies, will be decisive factors in accelerating 3D printing’s adoption.

Ultimately, with the current effort from the industry players and the tremendous pace of progress in this field, we’re excited about the impact 3D printing will have on manufacturing in the years to come.

.svg)

Subscribe to our

newsletter