The Evolution of 3D Printing Materials Market: Trends and Opportunities in 2019

The market for 3D printing materials is growing rapidly. Demand is increasing, with more companies buying additive manufacturing (AM) hardware and scaling their AM usage. In 2019, the AM materials market is valued at $1.5 billion. In the next five years, it’s expected to grow into a whopping $4.5 billion opportunity.With such an opportunity at hand, material suppliers, particularly giant chemical companies and metal producers, are becoming increasingly involved in the industry. Alongside developing new materials, they are contributing heavily to the industrialisation of AM. In today’s article, we’ll delve into how the 3D printing materials market is evolving in 2019, what companies are driving it and what trends are shaping its future. Take a look at the other articles covered in this series: How the 3D Printing Hardware Market is Evolving in 20193D Printing Software: Achieving True Digital ProductionPost-Processing for Industrial 3D Printing: Key Trends You Should Know

Polymers are the most used 3D printing materials

Polymers remain the leading 3D printing materials segment in terms of market share. From 2014 to 2018, 80.6% of global revenues for 3D printing materials came from polymers and reached $3.4 billion in 2018. According to recent Jabil’s survey of 308 3D printing users, 74% used polymer materials in 2018. The high demand for polymers is unsurprising. Polymer 3D printers have the largest installed base, as they are easier and cheaper to adopt and operate.

An increased focus on high-performance thermoplastics

While relatively simple plastics, like PLA and ABS, dominate the polymer market, there is a growing demand for strong, functional materials, which can withstand harsh environments and high temperatures. The 3D printing industry is responding to this trend by developing high-performance thermoplastics, like carbon-reinforced composites, ULTEM, PEEK and PEKK.

![Carbon PEEK 3D-printed part [Image credit: Roboze]](https://cdn.prod.website-files.com/68ada093f042e50f43548e00/696bd8fb0f1c439950b9614e_Roboze-Carbon-peek_edited.avif)

These materials enable manufacturers to 3D print functional prototypes and even end-use parts for a range of industrial applications.Across the industry, chemical companies are increasingly developing these advanced materials, specifically for use in AM, including Victrex, SABIC, Solvay and Evonik, to name a few. Many 3D printer hardware manufacturers are also working closely with these companies to adapt the 3D printing hardware required for these materials. For example, Roboze, an Italian manufacturer of extrusion 3D printers, has collaborated with SABIC on an amorphous thermoplastic polyimide filament, called EXTEM AMHH811F. The new material boasts great resistance to high temperatures, thanks to a heat deflection capacity of up to 230° C. The material also has a 247° C glass transition, which the partners believe to be the highest of any 3D printable material. Additionally, it offers excellent flame- retardant properties, good chemical resistance and maintains its mechanical strength at high temperatures. The development of high-performance thermoplastics is crucial for industrialisation of AM. They support the transition of the technology from prototyping to advanced applications in critical industries like medical and aerospace. For example, PEEK 3D printing is now used to create patient-specific implants. Perhaps a high growth opportunity in medical PEEK 3D printing has encouraged Evonik recently to invest in Meditool, a Chinese start-up specialising in PEEK 3D-printed implants for neurological and spinal surgery.The rise of composite materials Composite materials is another area of high-performance polymers seeing significant growth. Composites are made up of a thermoplastic matrix and reinforcing fibres. Presently, composites for 3D printing are reinforced with carbon fibres, glass fibres or Kevlar fibres.These materials, available as powders, pellets or filaments, most commonly feature chopped fibres, though continuous fibre composite printing is being explored more and more. For example, Desktop Metal has recently announced the Fiber 3D printer capable of reinforcing nylon, PEEK and PEKK materials with continuous carbon fibres.

A SmarTech Analysis report predicts that the global composite 3D printing market will grow at a CAGR of 22.3% over the next five years. This indicates a high value-generating opportunity, as composites become even more relevant in segments which expand beyond the medical and aerospace sectors and into consumer areas, such as next-generation automotive, energy, and transportation in general. The composite 3D printing market has been evolving over the last 12 months, with a number of materials and applications growing significantly. For example, composite 3D printing has enabled the launch of a composite 3D-printed bicycle frame. Earlier this year, Continuous Composites teamed up with Arkema, through the chemical giant’s Sartomer business line. The partnership will see Continuous Composites’ patented continuous fibre 3D (CF3D) printing technology, combined with Arkema’s photocurable resin solutions, thus providing new options for continuous fibre composite AM.In a similar vein, Sandvik has created the world’s first diamond composite for 3D printing. The composite demonstrated exceptional hardness and heat conductivity, as well as low density, corrosion resistance and good thermal expansion. Materials like this one could be particularly beneficial for space applications. 3D printing grapheneIn addition to engineering and composite plastics, the industry is working to enable 3D printing of advanced materials based on graphene. Graphene is one of the earth’s strongest materials. Due to its high electric and thermal conductivity, it is sought by a variety of industries, from battery manufacturing to aerospace. Last month, Terrafilum, a producer of 3D printing filaments, partnered with XG Sciences, designer and manufacturer of graphene nano-composites, to develop graphene-enhanced materials for extrusion 3D printing. Furthermore, researchers from Virginia Tech and Lawrence Livermore National Laboratory have been developing a novel way to 3D print complex objects, using graphene, since 2016. Previously, researchers could only print this material in 2D sheets or basic structures. Now they’ve developed a stereolithography-based process that can create small (down to 10 microns) graphene 3D structures. One company, however, was able to move 3D-printed graphene into a real-world application. American multinational engineering firm, AECOM, has used large-scale 3D printing from UK’s provider, Scaled, to create a 4.5 m-high signalling arch for transport networks.Using a graphene arch that sits over rail tracks eliminates the need to attach new digital equipment to existing infrastructure. The arch is produced in a new graphene-reinforced polymer, which is supplied by Aecom’s materials partner, Versarien.Despite this milestone, graphene remains a very challenging material to 3D print, and it’s also expensive and difficult to produce. In light of this, we’re still in the very early stages of graphene 3D printing - however, the progress so far looks very promising.

The explosive growth of elastomeric materials

Increasingly, companies apply 3D printing in consumer, medical and industrial applications, which require soft and flexible, yet tough and strong, properties. This demand fuels the growth of the market for flexible materials, like TPU and silicone. In just over the last six months alone, there’ve been several announcements around flexible materials for 3D printing. In July, global chemical company, Huntsman, introduced its range of soft, flexible IROPRINT AM materials for footwear applications. Materials come in three forms - resin, powder and filament - and can be used to produce footwear, hoses and gaskets, robotic grippers, seals and other rubber-like applications.Then German chemical company, Covestro, spotlighted a new application for its TPU material: 3D-printed orthopaedic insoles. [caption id="attachment_12045" align="aligncenter" width="800"]

![An insole 3D-printed using TPU material [Image credit: Covestro]](https://cdn.prod.website-files.com/68ada093f042e50f43548e00/696bda69dc2329db5a4baf25_covestro-insole-3d.avif)

An insole 3D-printed using TPU material [Image credit: Covestro] [/caption]TPU is the material of choice for this application, thanks to its favourable range of properties. In particular, Covestro’s TPU products cover a wide range of hardness, which can be adjusted by changing the structure of an insole design. This means manufacturers can print shoe insoles that feature hard or soft contact areas, achieving ultimate customisation. Furthermore, Dow, a global leader in silicone elastomer science, launched two new liquid silicone rubber 3D printing materials. Recently, the company partnered with Nexus Elastomer Systems and German RepRap, to give 3D printing users the ability to 3D print silicone rubber parts in colour. The new and colourful capability is dependent on a combination of three key elements: Dow’s SILASTIC 3D 3335 LSR material, German RepRap’s Liquid Additive Manufacturing (LAM) 3D printer and a new dosing system by Nexus Elastomer Systems. With this capability, users can add a range of colours to their prints, without changing the mechanical characteristics or performance of the part.Finally, EOS has recently expanded its polymer material portfolio with the launch of a new flexible EOS TPU 1301 powder. According to EOS, the EOS TPU 1301 offers great resilience after deformation, very good shock absorption and very high process stability. The material is particularly suited for applications in footwear, lifestyle and automotive – including cushioning elements, protective gear and shoe soles.Clearly, the availability of flexible materials allows companies to unlock new applications and benefit from 3D printing in many more niches.

Polymers with flame-retardant properties

There’s a strong push within the industry towards materials with specific properties, with flame-retardancy being one of them.This trend is likely driven by the demand from industries with strict fire safety requirements, like transportation and electronics, which are beginning to use 3D printing to a greater extent. Among recent developments is DSM’s UL Blue Card-certified flame-retardant material, Novamid AM1030 FR, for extrusion 3D printers. The material has been developed from DSM’s Novamid technology and is certified as V0 (burning stops within 10 seconds on a vertical specimen) and V2 (burning stops within 30 seconds on a vertical specimen).DSM believes the material’s level of flame retardancy makes it suitable for application in the automotive and electronics sectors.Similarly, Cubicure, Markforged and CRP Technology have released their own flame-retardant materials. The materials from CRP Technology and Markforged are also composites, which make them desirable for a number of critical industrial applications. We believe the development of specialised polymer materials will continue, as companies find more and more uses for 3D printing. Another area that we expect will see high growth is polymers with greater Ultraviolet (UV) resistance, which will help to propel their applications in the automotive sector.

Ceramic materials

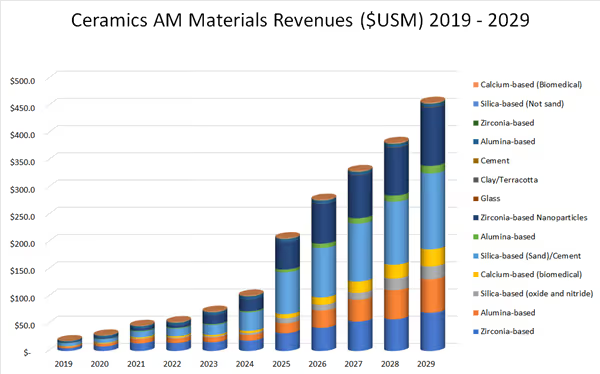

The 3D printing ceramics market is perhaps not yet as big as the polymer one, however, it’s equally exciting. This market is expected to grow from a $20 million revenue opportunity in 2020 to over $450 million by 2029, according to a report by SmarTech Analysis. The report also highlights the fact that the value of end-use parts, manufactured with technical or traditional ceramic materials, is expected to drive demand for hardware and materials for the medium to long-term future.

Technical, or high-performance ceramics, in particular, feature advanced mechanical properties, including very high strength, high temperature and chemical resistance. They are light materials, which are already used in several sectors of advanced manufacturing, from aerospace to electronics, many of which are among the first adopters of AM technologies. Last year, XJet Ltd., the company behind the NanoParticle Jetting (NPJ) technology for ceramics and metals, added a new ceramic material to its AM system: alumina. The new material joined zirconia in XJet’s portfolio of technical ceramics. Compared to zirconia, alumina shares certain features, such as higher degree of hardness and strength, but demonstrates lower wear resistance, making it easier to machine and refine before and after firing.Although ceramic 3D printing is lagging behind 3D printing of polymers and metals, there’s great potential for this technology and accompanying materials to evolve in the next five to ten years.

Metal materials

Metal AM materials is a sector full of growth. In 2018, revenue from metals reached 390 million EUR, as reported by Ampower, and grew an estimated 41.9%, continuing a streak of more than 40% growth for the last five years (Wohlers Report 2018). The number of companies adopting metal 3D printing is also steadily increasing, driving up the demand for greater material diversity and quality.

Metal powder production is going up

As a result of this demand, more and more material suppliers are joining the industry, and those who have already joined, are ramping up their metal production capabilities. This is especially common for metal powder producers, looking to supply materials for powder-based processes, like Selective Laser Melting (SLM), Electron Beam Melting (EBM), Binder Jetting and powdered Direct Energy Deposition (DED) - which are currently on a strong growth trajectory. One of the world’s leading manufacturers of metal powders, Höganäs AB, has begun the construction of its new atomising plant for the production of high-purity metal powders for the AM industry. The new plant located in Germany will help Höganäs to increase its market share in the growing segment of 3D printing. The powders produced at the plant will be sold globally, under the trademark Amperprint®. The Amperprint brand currently includes nickel, cobalt and iron alloys. Similarly, Liberty House Group, the parent company of UK’s Liberty Powder Metals, is building a powder metals development facility in the UK. The company hopes the facility will enable it to expand its reach in specialist metals and materials for AM. The plant will include capabilities like vacuum induction inert gas atomiser (VIGA) and a range of sieving, blending, packaging and analytical equipment. Furthermore, Sandvik, the developer and producer of advanced materials, has opened its new plant for the production of AM titanium powders through atomisation, in which it invested about 200 million Swedish Krona.Sandvik’s launch of a titanium powder facility supports a growing trend towards titanium 3D printing. Titanium can be a difficult metal to work with, particularly when it comes to machining. AM is becoming a viable alternative, helping companies to reduce titanium waste and provide greater design flexibility.

Metal material producers expand across AM value chain

Alongside increased metal powder production, many companies manufacturing materials for metal 3D printing are expanding their roles along the AM value chain. Some are strategically acquiring other firms, while others are restructuring their businesses. A great example of this is the British aerospace and automotive corporation, GKN. At the beginning of this year, its subsidiary, GKN Additive, announced a new sub-brand, GKN Additive Materials, formed as the result of a merger with GKN Hoeganaes, the parent company’s metal powder manufacturer.

This makes GKN Additive, which also has a sub-brand, GKN Additive Components, a full powder-to-part solution supplier. This allows the company to combine the knowledge of AM processes and materials under one roof, resulting in a better understanding of both aspects of AM technology. To further strengthen its position in the AM market, GKN has also recently acquired US-based 3D printing service provider, Forecast 3D. While Forecast 3D specialises in polymer 3D printing, this move will enable GKN to cross-promote AM now, both in metal and plastic. With this acquisition, UK-based GKN can have a greater reach across the US market and will be able to tap into a completely new line of business, which is polymer AM. And GKN is not the only example of expansion to other areas of AM. Swedish Sandvik has also recently made a surprising move by acquiring a 30% stake in Italian metal 3D printing service provider, Beam IT. According to the company, this move is in line with its strategic ambition to increase its presence in the wider manufacturing industry, a presence it hopes to achieve by investing in additive.

New metal materials for AM

With all these activities pointing to the healthy state of the metal AM industry, the ultimate indicator of its growth is ongoing material development. Metal powders are notoriously difficult to develop, let alone to certify. However, the progress in this area is continuous. For example, H.C. Starck Tantalum and Niobium GmbH, a subsidiary of JX Nippon Mining & Metals, has introduced a range of atomised tantalum and niobium (Ta/Nb) AM powders, under the AMtrinsic brand name.Thanks to its high melting points, high corrosion resistance and high thermal and electrical conductivity, these materials would enable AM users to apply the technology in chemical processing, the energy sector and a range of high-temperature environments. The AMtrinsic powders promise excellent flowability, high tap density, a ‘perfectly’ spherical shape and narrow particle size distribution - key characteristics for materials used in powder-bed fusion processes. Furthermore, OxMet Technologies, an alloy development company located in the UK, has developed a range of high-strength and high-temperature nickel alloys, designed specifically for the AM process.The new alloys are said to exhibit high strength up to 900° C. This is reportedly a significant performance improvement, as the strongest nickel alloy (Alloy 718) currently available for AM becomes unstable above 650° C, making it unsuitable for use in the most critical turbomachinery components.In another example, Aeromet International, a UK-based foundry specialist, enhanced its patented A20X aluminium powder, so that it’s surpassed the Ultimate Tensile Strength (UTS) mark of 500 MPa. According to the company, this achievement makes the material one of the strongest aluminium AM powders commercially available.To contribute to the idea of the circular economy, which is aimed at the continual use of resources, a microwave plasma technology specialist, 6K, has launched AM powders derived from sustainable sources.The powders are produced using 6K’s unique UniMelt technology, which is capable of transforming machined millings, turnings and other recycled feedstock sources into premium powder for AM.In the future, 6K plans to create powders from AM support structures and failed AM prints. The goal is to use 100 % of the materials that enter the supply chain, providing AM end-users with a new way to manage project costs and control supply chain, while also introducing greater sustainability in metal AM.

Materials: A crucial piece to the Additive Manufacturing puzzle

Materials play a critical role in making AM a true production technology. According to a recent survey by Jabil, 41 % of surveyed AM users believe that introducing better materials would make the greatest impact on encouraging the mass adoption of 3D printing for production. And the industry is actively responding to the demand. Advanced polymers are being developed, as well as specialised metals. Material suppliers now understand far more about how to identify, optimise, manufacture and recycle materials for AM. At the same time, we see more players branching into new areas of material development, be it composites, silicones or ceramics. That said, high material costs remain one of the key bottlenecks to scaling the technology applications. Perhaps we’ll see material prices dropping soon, as the demand increases. However, this won’t happen overnight. Ultimately, the 3D printing materials industry seems to be flourishing, driven by both large companies and niche start-ups. We’re assured that this upward trend will continue to shape the AM industry in the years to come.

.svg)

Subscribe to our

newsletter