How the 3D Printing Hardware Market is Evolving in 2020

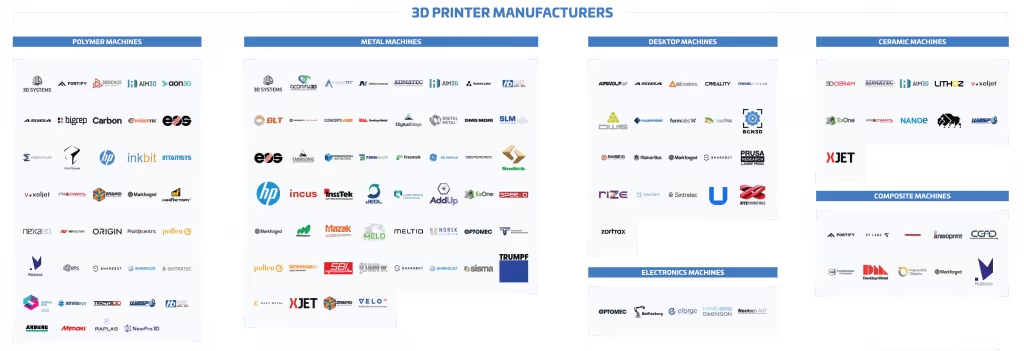

Earlier this year, AMFG published its second Additive Manufacturing Landscape 2020 report, looking at the key market players and biggest trends shaping the industry. Today, we’re launching a series of articles, taking a deeper dive into each segment of the additive manufacturing (AM) ecosystem, beginning with hardware. In 2020, hardware manufacturers make up more than half of the AM landscape, with a large number of them having joined the industry over the past decade. With the influx of new companies, recent years saw a rapid evolution of 3D printers, as they are becoming faster, more reliable and production capable. [caption id="attachment_13968" align="aligncenter" width="840"]

The AM Hardware manufacturers [Image credit: AMFG's Additive Manufacturing Landscape 2020] [/caption]Below, we’re tracing some of the most prominent developments and trends shaping the 3D printing hardware market. Take a look at the other articles covered in this series: The Evolution of 3D Printing Materials Market: Trends and Opportunities3D Printing Software: Achieving True Digital ProductionPost-Processing for Industrial 3D Printing: Key Trends You Should Know

Metal 3D printing hardware

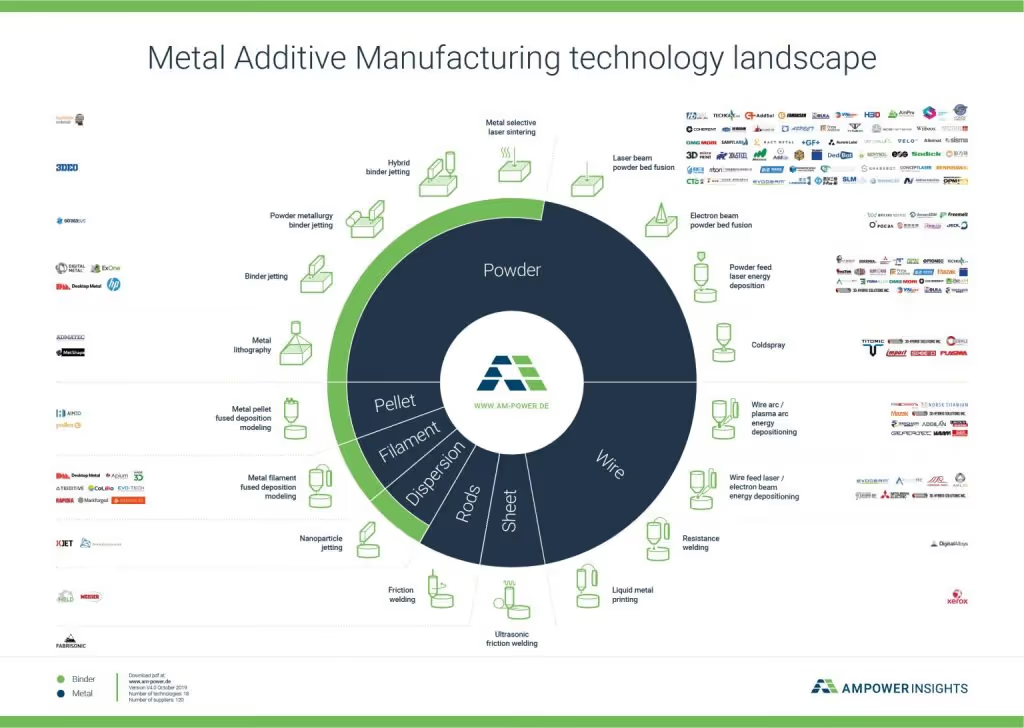

Arguably, the metal hardware market is one of the fastest-growing segments of 3D printing. Research firm, CONTEXT, estimates that metal 3D printer shipments will see year-on-year unit-volume growth rates of over 49 per cent. The metal AM hardware segment is also set to create an almost $4 billion revenue opportunity, according to a recent report from industry analyst firm, SmarTech Analysis.In 2020, the metal 3D printing market is extremely diverse, with as many as 18 different technologies shaping it, as reported by AMPOWER.[caption id="attachment_11720" align="aligncenter" width="840"]

[Image credit: AMPOWER] [/caption]Among these technologies, the Powder Bed Fusion (PBF) family plays the largest role in metal AM, comprising 80 per cent of all metal AM system installations worldwide. The PBF family encompasses laser-based and electron beam-based technologies. The PBF hardware market is divided among a few established companies, including EOS, Renishaw, 3D Systems, SLM Solutions, Trumpf and GE. GE, in particular, stands out with its unique diversification of offerings in the metal AM market. In addition to providing laser-based Concept Laser 3D printers, GE is also one of the very few companies offering Electron Beam Melting (EBM) equipment, manufactured by Arcam. Furthermore, the company is also developing metal binder jetting 3D printing, already adopted by a few early users. With the focus of metal 3D printing shifting toward production applications, many players in this field have been evolving their systems to meet the demand for faster speed and greater reliability. One of the common themes in this race is the introduction of multilaser systems. Using several lasers (usually 2 or 4) can speed up the printing process by increasing it as much as fourfold. Furthermore, multilaser systems are more productive, which helps to lower the cost of the part and/or produce more parts in a shorter period of time. It’s also claimed that multilaser machines can enable several parts to be printed at once.Among the 3D printer manufacturers offering such systems are EOS, Concept Laser (GE), SLM Solutions, Renishaw and Additive Industries. Outside of the established players, the PBF market saw the number of newcomers increasing, each with its unique take on the technology. One example includes VELO3D, which has developed a system that can print with almost zero supports, thanks to the advanced recoating mechanism and tight integration between hardware and software. Aurora Labs is another potential game-changer, offering a metal system that can print multiple layers of powder, simultaneously, in a single pass. Essentially, this equals a substantial improvement in print speed. Recently, the company has reported that its PMP1 3D printer can reach a print speed of 350 kg/day.

The rise of metal binder jetting technologies

Another noticeable trend is a new focus on metal binder jetting. While the technology has been around for a while, only recently has it been recognised as a viable method for high-volume applications. For one, metal binder jetting systems are typically cheaper and faster than PBF systems. ExOne, the first manufacturer of metal binder jetting systems, now has to compete with a number of newcomers like Digital Metal, Desktop Metal and HP. [caption id="attachment_9833" align="aligncenter" width="840"]

Dekstop Metal's Production Systems [Image credit: Desktop Metal] [/caption]Desktop Metal and HP, in particular, have an aggressive strategy in making binder jetting a method that can compete with traditional manufacturing for certain applications. To achieve this, Desktop Metal, for example, has developed a bi-directional system (prints in two directions), which enables high-resolution printing at up to 12,000 cm3/hr. This translates into over 60 kg of metal parts per hour. HP, on the other hand, has developed an innovative binding agent to make the sintering process, which takes place when parts are printed, faster and cheaper.‘With metal injection moulding you typically have more than 10 % by weight binder that has to be burned out. In our case, we have less than 1 %, which an order of magnitude is less, making it faster, lower-cost and much simpler to sinter’, says Tim Weber, HP’s Global Head of Metals, speaking in an interview with AMFG.Metal binder jetting has the potential to unlock the applications, currently unfeasible with other metal 3D printing technologies, particularly in high-volume industries like automotive. This means that the evolution in this sector will continue, making it the one to keep an eye on.

Compact metal 3D printers: A new segment full of growth

While PBF and metal binder jetting systems are designed to meet production needs, another sector of compact metal 3D printers is rising to make prototyping of metal parts cheaper and easier. A recent report from SmarTech Analysis predicts that the sales of compact industrial metal printers will top $1 billion by 2027. Markforged and Desktop Metal are currently the two biggest companies developing compact metal 3D printers.Both Markforged’s Metal X and Desktop Metal’s Studio System are extrusion-based 3D printers that use plastic-encapsulated metal powders to create green parts, which are then sintered in a furnace. This approach makes it a much more affordable option compared to traditionally more expensive metal 3D printers. This is largely due to lower operating costs, enabled by cheaper metal injection moulding materials.Affordability and easier set-up of compact metal AM systems is clearly resonating with the market. In Q1 2019, Markforged and Desktop Metal took the centre stage in terms of 3D printers shipment, with Desktop Metal shipping the largest number of metal 3D printers over the period. We expect that this segment of metal 3D printing will continue to grow, as compact 3D printers can tap into an entirely new market of affordable metal prototyping and product development. This also means that industrial customers have now more options than ever to aid in their exploration of metal AM.

Increasing reliability of metal 3D printing

To further advance metal 3D printers, companies need to introduce a higher level of repeatability to the process. The key solution to this lies in powering 3D printers with sensors and machine vision to enable in-process monitoring. Sensors and cameras, placed inside a 3D printer, can be used to measure multiple aspects of a build in real-time, helping to document the build process and ensuring requirements are met. The data obtained from sensors can then be fed back into specialised software, which will analyse the data and then provide feedback on how the process can be improved.This solution is known as a closed-loop control system, and it’s becoming an essential requirement for metal 3D printers. Maintaining control over the build process, through the closed-loop control system, enables manufacturers to achieve consistent geometries, surface finishes and material properties that underpin quality. However, in-process quality control, enabled by a closed-loop system, is still relatively new to AM technologies and presents a barrier for manufacturers to implement. As of 2019, only a small percentage of 3D printers, available on the market, are equipped with closed-loop control units.In the future, we anticipate that all metal 3D printers will be equipped with the closed-loop control system, which will significantly increase process repeatability, by reducing the risk of build failures.

Polymer 3D printers

While metal 3D printing hardware is growing rapidly, polymer hardware remains the biggest segment in terms of systems in use. 72 per cent of companies, surveyed for EY’s Global 3D Printing Report 2019, are using polymer AM systems, compared to 49 per cent that use metal ones. Less complex workflow and greater affordability are the two key factors for choosing polymer 3D printers over metal 3D printers.[caption id="attachment_11721" align="aligncenter" width="600"]

![Over the last decade, the polymer 3D printer market has seen a sharp increase in the number of companies. This was, in part, helped by the expiration of key patents around the same time [Image credit: AMFG]](https://cdn.prod.website-files.com/68ada093f042e50f43548e00/696bda58ce1e13cb21511f60_Number-of-Polymer-3D-Printer-Manufacturers.avif)

Over the last decade, the polymer 3D printer market has seen a sharp increase in the number of companies. This was, in part, helped by the expiration of key patents around the same time. [Image credit: AMFG] [/caption]Similar to the metal 3D printing market, the polymer market is divided by a number of technologies, including Fused Filament Fabrication (FFF), Stereolithography (SLA)/Digital Light Processing (DLP), Selective Laser Sintering (SLS) and Multi Jet Fusion (MJF), with many new technologies awaiting commercialisation in the next few years. Each of these technologies is undergoing an evolution, as companies are aiming to develop reliable, professional solutions, both for production and prototyping. Perhaps the most impressive developments are taking place in the SLA/DLP hardware segment. These technologies are becoming true production solutions, especially for industries like dental and consumer products. For example, SLA 3D printers are used to produce the majority of moulds for dental clear aligners, churning out hundreds of thousands of devices per year. However, the technology still needs to mature in order to go beyond just moulds and enable direct production of such devices.When it comes to the hardware with the largest installation base, FFF 3D printers remain on top. This can be explained by the popularity of accessible desktop FDM 3D printers from companies like Ultimaker and Makerbot.

Exciting developments in SLS 3D printers

Moving on to SLS 3D printers, this sector has also seen some notable developments. One example involves Aerosint, a Belgian company, which is working on an SLS system that will be able to print with two different powders. This will allow the machine to use one powder as an inexpensive support material. Normally, the unfused support powder in an SLS machine is the same material used to print a part, and it tends to be expensive. Introducing a machine that can use cheap support material and a second material for part printing, could save a significant amount of money for those using SLS processes. Another development that can reimagine SLS 3D printing comes from EOS. At Formnext 2018, EOS premiered an upcoming LaserProFusion system that promises to make the polymer 3D production 10 times faster. To achieve this feat, the company spent more than 8 years on reimagining the laser technology used in the process.[caption id="attachment_9572" align="aligncenter" width="840"]

EOS's LaserProFusion technology will be equipped with up to

a million of diode lasers to enable faster SLS 3D printing [Image credit: EOS] [/caption]While current SLS machines use one, or a few, CO₂ lasers, the LaserProFusion system will be able to use up to a million diode lasers. This will allow it to create parts, not only with high resolution, but also at a much greater printing speed, potentially rivalling injection moulding.The technology is slated for commercial release in the next few years.

The fast growth of HP Multi Jet Fusion

MJF entered the market in 2016, when HP publicly unveiled its move into 3D printing and launched its first polymer 3D printer. Since then, MJF has become one of the fastest-growing polymer 3D printing processes. More than 10 million parts are said to have been produced using HP’s MJF 3D printers in 2018. MJF, which belongs to a powder bed fusion family like SLS, has advantages when it comes to dimensional accuracy and material properties, making it possible to print high tolerance parts that are superior in both strength and flexibility. HP is committed to advancing MJF technology . Last year, it launched a Jet Fusion 5200 Series. This new Series expands upon HP’s existing MJF portfolio, which also includes the Jet Fusion 300/500 Series for functional prototyping and the Jet Fusion 4200 Series for short runs and production. The new 3D printer series adds to the portfolio, offering a solution for volume production.[caption id="attachment_11722" align="aligncenter" width="780"]

HP's new Jet Fusion 5200 3D printers for production applications. [Image credit: HP] [/caption]Among the most notable features of the 5200 Series is the upgraded power of lamps inside 5200 3D printers. This enables the new system to fuse powder in a single pass, as opposed to a two-pass mode in the previous systems. As a result, the system has 40 per cent improvement in productivity and opens up possibilities for 3D printing of high-temperature materials.

Professional desktop 3D printers

The desktop 3D printing market is one of the youngest within the hardware sector. Its emergence can be traced back to the beginning of ‘the maker movement’, at the end of the 2000s. The movement brought forth the consumer 3D printing revolution, which, however, quickly collapsed due to the lack of demand in the consumer market. The burst of the hype surrounding consumer 3D printing forced many desktop 3D printer companies out of business. However, a few have survived by transitioning from the consumer to the professional and enterprise market.This allowed vendors like Ultimaker, MakerBot and Formlabs to move in, grow and thrive. This shift has also revealed a growing need for industrial systems that are smaller and a fraction of the cost of their larger counterparts. Shifting the focus towards the professional users, required desktop 3D printer vendors to revamp their solutions. This resulted in the introduction of industrial features that were previously found only in high-end 3D printers. For example, a heated bed, an enclosure and a dual extruder have become the necessary elements of FFF desktop 3D printers, targeting professional application. Generally, companies have been trying to make systems more productive and reliable while maintaining a compact format. Considering desktop SLA, Formlabs remains one of the leading companies in this sector. It claims to be the world’s largest seller of desktop SLA 3D printers, with more than 40,000 systems sold.[caption id="attachment_11723" align="aligncenter" width="840"]

Form 3 and Form 3L 3D printers [Image credit: Formlabs] [/caption]In 2019, Formlabs introduced a new technology, called Low Force Stereolithography (LFS). The LFS process offers improved detail and surface finish, thanks to its flexible tank that is said to reduce forces on parts while printing. Built on the advanced LFS technology, Formlabs’ new Form 3 and Form 3L 3D printers are helping to bridge the gap between desktop and industrial-grade 3D printing.

Ceramic 3D printers

In 2020, ceramic 3D printing is not as well established as polymer and metal 3D printing technologies. The technology is still in the early stages of development, although it’s predicted to reach maturity within the next 5 to 6 years. Due to the novelty of the technology, there’s a handful of vendors offering systems for 3D printing of ceramics. Among them are 3D Systems, ExOne, Prodways, Lithoz, 3DCeram and XJet. One development that could be particularly transformative for ceramic 3D printing, is the introduction of XJet’s Nanoparticle Jetting Technology (NPJ). [caption id="attachment_11724" align="aligncenter" width="840"]

XJet ceramic Carmel 1400 3D printer [Image credit: XJet] [/caption]Debuted in 2016, NPJ is a type of inkjeting where material nanoparticles (it can be ceramic or metal) are suspended in a liquid formulation. Then thousands of nozzles in the XJet system jet millions of ultrafine drops of these liquid suspensions, both the build and the support material. An XJet printer maintains the high temperature inside (up to 300°C) during the printing process. This helps to burn out the liquid as it’s deposited, resulting in a solid part. The part out of the printer, however, remains in a green state and needs subsequent sintering to complete the solidification. Inkjet 3D printing is well-known for its accuracy and the ability to achieve a high level of detail. It means that XJet systems are potentially capable of creating finished parts of almost any geometry, including those with tiny holes, thin walls, challenging arches and sharp edges.Applications like components for a new breast cancer treatment and 3D-printed antennae have already shown the suitability of XJet’s 3D printers for industrial applications. Despite recent progress, there’s still a long road ahead of ceramic 3D printing. However, as the demand for 3D-printed ceramic parts is growing, 3D printing of ceramic will ultimately become an important and profitable section of the manufacturing industry.

Electronic 3D printers

Like the ceramic market, the 3D printing market for electronics is still relatively young but is one that holds great promise. Currently, only a few companies are providing hardware for electronics 3D printing, with the likes of Nano Dimension and Optomec leading the charge. The technologies behind the Nano Dimension’s and Optomec’s systems are vastly different but offer an equally exciting opportunity for prototyping and direct production of electronic components, like antennae, Printed Circuit Boards (PCBs), capacitors and sensors. One development that has generated a lot of attention recently, involves the introduction of DragonFly Lights-Out Digital Manufacturing (LDM). [caption id="attachment_11725" align="aligncenter" width="780"]

The DragonFly Lights-Out Digital Manufacturing (LDM) 3D printer [Image credit: Nano Dimension] [/caption]The system builds on the Nano Dimension’s DragonFly Pro system, which was launched back in 2017, to allow engineers and designers to quickly prototype electronic components. The LDM is said to push these capabilities beyond prototyping, to deliver in-house, around-the-clock manufacturing for short run of small batches of parts. Like earlier versions of the Nano Dimension’s 3D printing systems, this system works by co-depositing conductive and insulating materials on a PCB substrate. What’s different, however, is the productivity of the machine, which was increased by more than 40 per cent, compared to the DragonFly Pro. Advancements like this one are encouraging, as they help to push the envelope for electronic 3D printing, beyond prototyping. While there’s still much to be done, not only in terms of hardware but also materials and software, it definitely sets the foundation for electronic 3D printing to reach maturity.

3D printing hardware: Achieving ultimate reliability

The 3D printing hardware sector is evolving rapidly, as companies are constantly improving upon the available systems and developing entirely new hardware solutions. That said, the cost of equipment remains one of the biggest deterrents to investing in AM. According to the EY Global 3D Printing Report 2019, 87 per cent of companies see high systems’ prices as a critical barrier to 3D printing adoption. This means that lowering the cost of AM equipment will be key to expanding the use of the technology. The 3D printing industry is solving this issue by introducing more accessible desktop 3D printers and compact metal AM machines.In the meantime, it's clear that the 3D hardware industy has been affected by the outbreak of the pandemic, with shipments seeing unsurprising drop. Market research firm, CONTEXT, indicates that hardware revenues in the overall 3D printer market are down by -27 per cent from last year’s figures . Almost all Western top 20 industrial printer companies saw sizable year-on-year declines in the number of 3D printers shipped. That said, 3D printing vendors have been reporting renewed interest in the technology throughout Q3 – from new sectors as well as known markets. According to CONTEXT, they are hopeful that this interest will turn into Q4 orders.All in all, the demand for more sophisticated industrial-grade systems will continue to fuel the evolution of the AM hardware. In the next five years, we expect 3D printing hardware to reach much greater reliability, thanks to in-process monitoring solutions and tighter integration with software.

.svg)

Subscribe to our

newsletter