Has 3D Printing Reached the Plateau of Productivity?

[Image credit: BMW Group]

In the Gartner Hype Cycle – a graph that measures technology’s maturity – the plateau of productivity represents a stage when mainstream adoption starts to take off. But where does 3D printing stand on this graph? In other words, can we say that it has reached maturity?

The 3D printing industry is vast: there are multiple segments with varying degrees of maturity. That said, we can still capture several trends indicating that 3D printing is coming of age.

We take a look at them below, as well as dive into the three sectors of 3D printing that show signs of early mainstream adoption.

[toc]

A steadily maturing 3D printing industry

Several trends and developments indicate the industry is on its way to maturity. Below, we analyse the uptick in M&A activity, the expanding uses of 3D printing fuelled by technology advancements and the desire for greater integration and interoperability.

The wave of consolidation

Most new industries are fragmented, and consolidate as they mature. According to the Consolidation Curve framework, all industries follow a similar life cycle through the 4 stages of: Opening, Scale, Focus, and Balance & Alliance.

Using the framework and the history of 3D printing as guidance, we can gauge where the industry stands on the consolidation curve.

Appeared in the 1980s, 3D printing had been going through the opening stage up to the end of the 2000s, with companies like Stratasys, 3D System, Materialise creating a global footprint, and establishing barriers to entry by protecting proprietary technology.

The beginning of the 2010s marked a transformational period for 3D printing that was entering the next stage of the Consolidation curve – Scale. The industry was growing exponentially. The new major players were appearing, like MakerBot, 3DHubs, Formlabs to name a few. And the number of acquisitions was accelerating, led primarily by Stratasys and 3DSystems.

But the industry was also accumulating a lot of hype around it. When the hype cycle bottomed out around 2015, many predicted the end of the 3D printing industry.

However, what’s ended in reality was the consumer interest. The end of hype revealed the true nature of 3D printing as manufacturing technology with huge potential across many industries.

While the Scale stage of consumer 3D printing dwindled, the Scale stage of industrial 3D printing flourished.

Going into the 2020s, we’re starting to shift from the second Scale stage to the third Focus stage – and the last 12 months only highlighted this trend, with a notable uptick in large-scale M&A activity.

Among some of the highest-profile 3D printing M&A moves in the last months have been:

- Stratasys acquiring Origin

- Stratasys acquiring RPS

- Desktop Metal acquiring EnvisionTEC

- DSM acquiring parts of Clariant’s 3D printing portfolio

- Covestro acquiring DSM Resins & Functional Materials line of business, including DSM Additive Manufacturing

- Protolabs acquiring 3DHubs

- BEAMIT Group acquiring 3T Additive Manufacturing

- Nikon purchasing a majority stake in Morf3D

The key strategies behind the increase in M&A in 3D printing include:

- Manufacturing businesses wanting to expand their reach (Nikon & Morf3D);

- AM companies enhancing their position along the value chain (e.g. Desktop Metal & EnvisionTEC);

- AM equipment manufacturers absorbing innovative technologies (e.g. Stratasys & Origin).

That said, the 3D printing industry is still years away from the last stage of Balance & Alliance, whereas only a few industry titans reign, accounting for as much as 70% to 90% of the market.

As it looks now, the 2020s will be marked by the megadeals trend, which will reshape the 3D printing industry and reposition it on a global scale.

Uses of 3D printing beyond prototyping are increasing

Since its emergence, 3D printing has been primarily used for prototyping, slashing time-to-market and enhancing product development. However, over the last few years, we’ve been noticing a shift in usage, with the percentage of 3D-printed end-use parts increasing.

This trend is highlighted by several industry surveys. For example, Ultimaker’s 3D Printing Sentiment Index 2021 reported a 7% decrease in prototyping applications, whereas the end-use part usage increased by 5% compared to the 2019 results.

Jabil’s 3D Printing Technology Trends 2021 report tells a similar story. The survey states that while prototyping remained flat, the use of 3D printing for end-use parts has been on a growth trajectory. Almost 55% surveyed companies say they use at least a quarter of their 3D printing capability to produce functional or end-use parts – a notable growth compared to 2019’s numbers.

These figures signal that AM has reached the inflexion point, evolving from a technology for enthusiasts and early adopters to a technology with a broad range of industrial applications. In other words, the adoption of AM has reached another level – the level of early maturity.

High-speed 3D printing and the expanding material choice

The rise of 3D printing for functional applications is closely tied to the advancements in materials and hardware.

Compared to traditional manufacturing, most 3D printing processes were slow and lacking functional, certified materials for production applications.

3D printing industry players, envisioning the disruption of the traditional manufacturing industry via AM, had to find a way to industrialise 3D printing.

This meant developing technologies that support higher production volumes, and materials that enable advanced AM applications.

As a result, on the hardware side, we’re witnessing the rise of binder jetting and multi-laser powder bed fusion for metals and vat photopolymerisation processes for plastics.

In the meantime, materials brands are increasingly focusing on high-performance materials, including advanced alloys and composites.

Read also: Composite 3D Printing: An Emerging Technology with a Bright Future

Ultimately, shifting the focus on production-capable solutions helps to boost the growth of AM in industry sectors that were previously hesitant about adopting 3D printing for functional applications.

Creating an integrated AM ecosystem

AM, as an Industry 4.0 technology, can reach maturity only by removing silos across its operations and supply chains.

While much of the focus in AM remains on hardware and materials, there is more and more emphasis on creating an interconnected, automated ecosystem.

This trend is evident on multiple fronts, from design automation through topology optimisation to post-production automation that removes much of the complexity and manual labour.

On the production management side, specialised additive MES software has appeared to automate order handling and production scheduling processes

Further reading: Solving additive manufacturing challenges with MES

Another crucial step in automation comes from hardware manufacturers that are opening up their systems for integration with third-party software. Improving connectivity between AM systems and software solutions will ultimately help to create an integrated ecosystem that supports interoperable, scalable additive manufacturing.

The plateau of productivity: What 3D printing segments have reached it?

While the 3D printing industry is maturing, the progress across its different segments is not uniform.

Some sectors of 3D printing are still in the early stages, like 3D-printed human tissues, while others are nearing the maturity stage, like 3D printing with polymers.

But what are the other segments that are climbing the plateau of maturity and what is driving their growth?

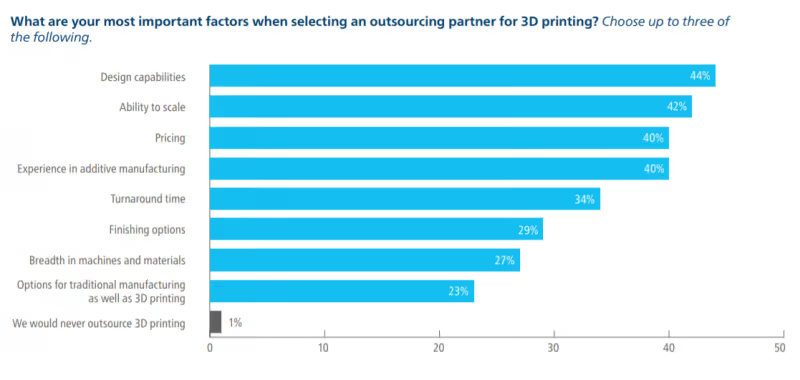

3D printing service providers

Some quick facts about the AM services industry:

- The Wohlers Report 2021 states that 3D printing service providers generated a whopping $5 billion in revenue in 2020;

- According to the EY Report 2019, service providers make up 34% of the global AM landscape;

- Around 45% of companies outsource 3D printing jobs, as reported by Jabil 3D Printing Trends Report 2021.

While the 3D printing industry experienced an overall decline in 2020, the services business continued to grow. Many, if not most, companies, get familiar with 3D printing through service providers.

With the recent supply chain shocks, companies started to investigate the benefits 3D printing can provide for their supply chains – and service providers became the initial touchpoints for many to learn and understand the technology.

However, the competition in the 3D printing service industry has increased in sync with the overall sector growth.

On the one hand, hardware manufacturers and materials companies are launching AM services business lines, or expanding them through acquisitions. On the other hand, a Manufacturing-As-A-Service business model, that links buyers and suppliers through a single site, has been booming.

In such a competitive landscape, service providers must constantly innovate, by diversifying their service offerings, standardising and automating their processes and by tapping into new markets.

Dental 3D printing

The introduction of high-speed polymer AM technologies has significantly boosted the growth of 3D printing in dental.

As estimated by the market research firm SmarTech, the AM dental and medical industry has topped $3 billion.

Digital dentistry – the introduction of digital technologies into the dental practice – has become a common trend in dentistry. And 3D printing is one of the key technologies, alongside intraoral scanning, that’s driving this trend.

3D printing has many applications in the dental industry, including bridge models, surgical guides and dentures. However, the manufacturing of clear aligner models is one of the most common uses of dental 3D printing today.

According to SmarTech Analysis, clear aligners are “perhaps the single highest volume application for 3D printing technologies in the world today.”

3D printing accelerates the process of creating patient-specific clear aligners by enabling hundreds of custom moulds to be produced directly from patients’ digital scans in one batch.

No other technology would be able to create that amount of customised moulds in such a fast and cost-effective way, other than 3D printing.

3D printing has proved to be a game-changer for dental, offering a solution that can make fixing teeth cheaper, faster, and widely available to customers.

It’s therefore unsurprising that over 70% of dental labs in the US are predicted to own 3D printing technology by the end of 2021, with dental 3D printing becoming a $9.2 billion industry in the next five to seven years.

Metal powder bed fusion

Metal 3D printing encompasses many technologies, but one of the most matured among them remains metal Powder Bed Fusion (PBF).

Over the last decade, metal PBF 3D printer manufacturers have been working hard on optimising the technology for production. To this end, we’ve seen key market players launching solutions for automated and integrated production.

The majority of these solutions share similar characteristics: they are modular, configurable and offer a high level of automation in a bid to maximise efficiency and reduce the amount of manual labour required.

Thanks to these developments, laser PBF has found its way into many industries and applications. One industry that has been particularly keen on adopting metal PBF is aerospace.

Today, metal PBF 3D-printed parts are powering crucial aircraft and spacecraft systems like engines. This is where the technology’s key capabilities — the production of complex parts with simplified assembly and less material waste — truly shine.

As of now, laser PBF technology is capable of delivering functional parts repeatedly. However, it still requires some fine-tuning and testing before manufacturers can commit to full-scale production.

Going forward, the ease of use and reliability of metal PBF systems will increase, driven in many ways by the advancements in software and overall workflow.

One example supporting this trend comes from California-based metal 3D printer manufacturer, VELO3D.

When developing its metal PBF technology, called Intelligent Fusion, the company has put a key focus on software and hardware integration. The result is a tightly integrated system that can print parts with fewer supports, better surface finish and, reportedly, a higher success rate. This, in turn, leads to greater reliability, faster production and less post-processing.

Metal PBF remains the driving force of the metal 3D printing industry. Metal PBF 3D printers have the largest installed base amongst other metal 3D printing technologies. And PBF 3D printer manufacturers have the biggest shares of the metal 3D printing market when compared to companies producing other types of metal 3D printers.

On top of that, the use of metals in 3D printing has grown by 20% since 2019, while the use of polymers grew only by 12% – yet another stat heralding the growing confidence in metal 3D printing maturity.

Industrial 3D Printing: Entering a decade of sustained growth

The 3D printing industry has entered a new period of growth and industrialisation.

In todays’ complex environment, more and more companies are responding to constraints in their supply chain and manufacturing operations by looking to 3D printing.

For our industry, this means more developments across different segments of 3D printing, not only those I highlighted above.

Accelerated advancements in additive manufacturing will ultimately bring a vision of distributed digital manufacturing into reality. It has long been in the works and now it’s slowly taking shape, as all pieces of the AM ecosystem are gradually coming together.

How will the manufacturing industry look once the AM technology fully matures? I believe it won’t take us too long to learn.

Discover how you can lay the foundation that will fast-track the shift to distributed additive manufacturing in our free whitepaper.

.svg)

Subscribe to our

newsletter